FHSSS vs Traditional Savings: What’s the Best Way to Save for Your First Home in Australia?

In 2017, the Australian Government introduced the First Home Super Saver Scheme (FHSSS) to help first-time buyers save for a deposit through their superannuation. The idea is simple: take advantage of super’s tax benefits while building your home deposit.

You can contribute up to $15,000 per financial year, with a lifetime cap of $50,000 (per person), which can later be withdrawn — with earnings — to use as a deposit for your first home.

How Does the FHSSS Work?

It’s relatively straightforward:

- You make voluntary before-tax or after-tax contributions to your super.

- Once eligible, you apply to the ATO for a determination and release of your funds.

- You then have up to 12 months (with possible extensions) to use the released amount for purchasing or constructing your first home.

What Are Traditional Savings?

Traditional savings refer to putting aside money in a regular bank account.

Common options include:

- High-interest savings accounts.

- Term deposits.

- Offset accounts linked to a mortgage.

These methods offer simplicity and flexibility, with no super rules or government restrictions.

Key Differences: FHSSS vs Traditional Savings

Let’s compare them across several factors:

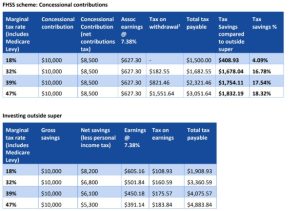

1. Tax Advantages

- FHSSS: Contributions are taxed at just 15%, compared to your marginal tax rate — potentially saving thousands.

- Traditional Savings: No upfront tax benefits. Interest may be taxed based on your income bracket.

2. Liquidity

- FHSSS: Funds are locked until the ATO releases them for a home purchase.

- Traditional Savings: Funds are accessible at any time, with no conditions.

3. Flexibility

- FHSSS: Must be used for a first home. Changing plans can complicate access.

- Traditional Savings: Use the funds however and whenever you like.

4. Capital Growth

- FHSSS: Funds may grow based on your super fund’s returns..

- Traditional Savings: Minimal growth, typically limited by low interest rates and inflation.

Benefits of FHSSS

- Tax Savings – Potentially thousands saved via concessional tax treatment.

- Disciplined Saving – Funds are harder to access, which can reduce temptation.

- Government Support – Backed and regulated by the ATO.

- Potential for Greater Growth – May outperform standard savings accounts.

Drawbacks of FHSSS

- Restricted Access – Funds are only available for home purchase.

- Complexity – Requires understanding rules, forms, and ATO processes.

- Investment Risk – Returns depend on your super fund’s performance.

- Time Limits – Must purchase within 12 months (extensions available).

Advantages of Traditional Savings

- Simplicity – Easy to understand and manage.

- Full Access – Available anytime, including for emergencies.

- Security – Bank deposits are guaranteed up to $250,000.

- No Red Tape – No ATO processes or paperwork.

Limitations of Traditional Savings

- No Tax Incentives – Standard interest income may be taxed.

- Low Returns – Often barely outpaces inflation.

- Easy to Spend – Liquidity can lead to impulsive use.

Which Builds a Bigger Deposit Faster?

For many, FHSSS can build a larger deposit thanks to the tax advantages and potential super returns — if you’re disciplined and committed to buying a home.

Ft-fhss-faq.pdf – reference link

Ft-fhss-faq.pdf – reference link

What Does FHSSS Offer?

- Contribute up to $15,000 per year

- Up to $50,000 total per individual

- Couples can combine for up to $100,000

Who Should Consider FHSSS?

- Individuals earning over $45,000 annually

- People with stable income and a clear home-buying plan

- Savers wanting to maximise deposit size using tax-efficient methods

When Traditional Savings Might Be Better

- You’re uncertain about buying soon.

- You need emergency funds or quick access.

- You’re self-employed and don’t contribute regularly to super.

Why Not Both? Combine FHSSS + Traditional Savings

Pro tip: Use both methods to your advantage.

- FHSSS for long-term, tax-effective growth.

- Traditional savings for flexibility and short-term needs.

This combination gives you tax benefits and liquidity in case your plans change.

Final Thoughts

For many Australians ready to purchase, the FHSSS offers a powerful edge in building a larger deposit. But if flexibility and ease are your top priorities, traditional savings still have their place. The smartest move? Combine both where possible to get the best of both worlds.

Conclusion

Saving for your first home doesn’t have to be overwhelming. The FHSSS brings excellent tax advantages, especially for higher earners. However, traditional savings offer the ease and freedom many people need. The real benefit comes from structuring your strategy around your goals — and if you’re not sure, a licensed financial adviser can help craft the right plan for you.

Leave a Reply